.png?width=214&height=69&name=JLAMlogo-white-outs%20(1).png "JLAMlogo white outs")

.jpeg "What are the Tailwinds Associated with Multi-Family Investments?")

Sophisticated investors pay attention to macro factors that provide favorable support for investment strategies. At JLAM, we look for trends, imbalances, and other drivers that can generate long-term tailwinds for a theme in developing our investment programs. Here are some dynamics we believe offer long-term tailwinds for the multi-family asset class.

Limited supply

Currently, the housing market is facing a significant deficit—the US is an estimated 6.5 million units short. While building permits in December 2023 came in at 1.46 million and are a 7.6% increase from the 1.36 million of December 2022, this level of housing production will not put a dent in the problem and may not be aligned with where housing needs are. Much of the new housing production is concentrated in a handful of markets, which can mask the shortage issue when looking at national figures.

This dynamic also does not account for high interest rates that are preventing current homeowners from selling (which is happening because people are avoiding giving up their locked-in low mortgage rates). Because of this, existing home inventory available for sale is extremely low—as of year-end 2023, it was just 3.2 months, far below the long-term average.

Source: National Association of Realtors®

Multi-family investments in markets that continue to experience a supply/demand imbalance are a way to capitalize on the shortage. The supply gap provides support for rental rates and helps provide stability in occupancy rates—both key elements in a successful investment.

Demographic shifts

The pandemic altered people’s living and location choices. With remote work a viable option, some people no longer feel they need to live near major metros. For example, Delaware ranks seventh in the US in terms of population growth rate. People are moving from California, New Jersey, and New York to more affordable states, particularly into our target areas—the Mid-Atlantic and Southeast regions, with North Carolina a particularly hot market.

Many of these people are choosing to rent rather than buy. For instance, AARP reports the number of renters 65 and older will increase from 7.4 million in 2020 to 12.9 million by 2040. Boomers feel downsizing and renting offer a less time- and labor-intensive option than ownership.

However, they are not the only generation who share this housing preference because of increasing desire for flexibility and mobility. RealPage finds 51% of Gen Zers believe renting is better than buying, and 66% of current renters are satisfied with their housing situation.

All generations enjoy renting because of several common aspects, with one being a desire for convenience. Whether it’s the empty nesters who want “less house” to worry about and no surprise maintenance costs, or professionals seeking quicker access to public transportation for their work commute, this factor drives a preference to lease instead of own.

Another important reason why people prefer to rent is the amenities multi-family developments offer. Living in a vibrant neighborhood that has a one-stop shop, so to speak, of most person’s needs—gym, pool, outdoor activities like tennis and pickleball courts, and walking or biking trails—allows people to feel fulfilled with their lives.

All these reasons contribute to steady demand for quality apartment living options, leading to strong occupancy rates and stable rents, which drives investor returns.

Economic stability and job growth

Even with remote positions, the majority of people still move to where there is work. Case in point—North Carolina is expected to add over 445,000 new jobs throughout this decade. This is a big reason—along with affordability—why people are flocking to the state, as cited earlier. Multi-family investments and developments support population growth by providing housing options that address residents’ living preferences.

Affordability

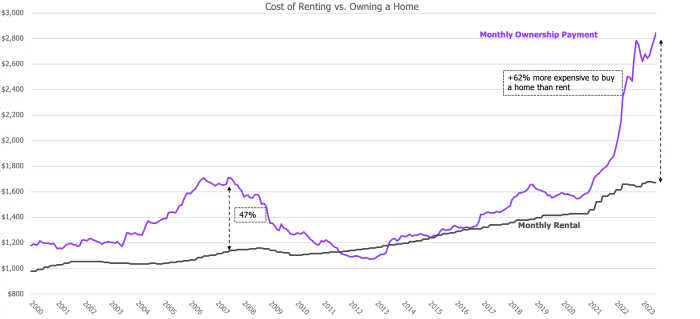

Rental preference does not necessarily acknowledge the biggest elephant in the room—home ownership affordability. RealPage’s survey finds their responders’ average household median income is $65,000, and 73% of these renters say they are in an area where they cannot afford to buy. With the median home price in Q3 2023 at over $400,000, it is no wonder tenants feel they cannot purchase their own house. Them Report points out, “During the past 12 months, with an average 30-year fixed mortgage rate jumping from 5.22% to 7.07%, the cost to buy a starter home in markets that favor renting climbed at an average rate of 21.4%.”

On the other hand, renters do not have to worry about down payments, monthly mortgage payments, property taxes, or maintenance costs. They are responsible solely for their rent and utilities, which MarketWatch reports was $2,052 in August of 2023. Compare that to the estimated median monthly mortgage payment to be $2,632 in September of last year, and you can see how keeping almost $600 per month in their bank accounts is a more attractive option.

Source: MarketWatch

Housing diversification

Investors are often advised to have a diverse portfolio to hedge against downturns. Real estate investors and developers are no different and seek to manage risk through using a mix of unit types. Multi-family inherently consists of multiple housing units within a single complex, which provides some diversification. If one unit is vacant, the other ones’ returns can cover it until a tenant is found.

This is expanded further by offering a variety of unit configurations—at its simplest, one-, two-, and/or three-bedroom apartments meet the needs of different segments of demand. Often you can see developers feature several styles of units within new developments. You may find a 300-unit community featuring 200 single-family homes with 100 townhomes, or a 280-unit development that has 200 traditional apartments and 80 townhomes. These approaches can provide built-in (pun intended) risk management because it fuels higher occupancy rates by addressing various housing preferences.

How multi-family investments benefit you

Besides the stable occupancy rates and potential for rental rate growth driven by limited supply, demographic shifts, economic factors, and housing diversification, multi-family investments can benefit investors in several additional ways. First, there are multiple approaches to investing in multi-family, each with their own risk/reward profile that may be suitable for different aspects of your portfolio. These include buy-and-hold for rental income and appreciation, value-add through renovations and improvements, and potential for economies of scale with larger property opportunities.

Another important element of multi-family investing is the availability of financing, as Government Sponsored Entities (GSEs), namely Fannie Mae, Freddie Mac, and HUD, provide attractive options that make it easier for investors to acquire multi-family properties and provide liquidity to the marketplace even when traditional lending is constrained. This is one of the reasons why multi-family has become such an attractive asset class. In fact, even during a markedly low period of transaction volume in real estate, multi-family investments were 35% of all deals in the second quarter of 2023.

Real estate investors may also receive various tax benefits like depreciation, deductions, and mortgage interest deductions. For example, multi-family properties can be analyzed using a cost segregation study that may enable the recognition of significant depreciation in the early years of owning an asset, often resulting in a taxable loss for investors. This generous tax break is just one of the many ways your long-term returns can be enhanced.

Finally, real estate investments in general—but specifically multi-family—can provide a hedge against inflation because lease durations are only one year (for apartments). Property values and rental income tend to increase over time, so the lease’s terms are readjusted year-to-year, providing a reliable long-term investment that keeps up with the value of the dollar.

Why JLAM?

Since JLAM was founded in 2011, we have identified major tailwinds that can impact real estate. We have designed investment strategies to capitalize on these key trends, and then we have surgically found the best opportunities within the targeted opportunity set. So, we have a rising tide and then we skillfully find the best boat among all the boats.

By using this approach, we have deployed over $400 million in capital since 2011, developing over 3,000 units and 1+ million square feet of commercial real estate—with much success specifically in the multi-family sector. We’ve delivered an average Net IRR over 19% and an average 1.9x Net Multiple, which has led to very satisfied investors as evidenced by our investor re-up rate approaching 100 percent.*

If you're interested in learning more about private multi-family real estate investments and our pipeline of exciting projects, schedule an appointment with us.

*All investments involve the risk of potential investment losses as well as the potential for investment gains. Prior performance is no guarantee of future results, and there can be no assurance, and clients should not assume, that future performance will be comparable to past performance. Metrics updated as of June 30, 2023. JLAM does not provide tax, legal, investment, or accounting advice. This website has been prepared for informational purposes only, and is not intended to provide, and should not be relied on for, tax, legal, investment, or accounting advice. You should consult your own tax, legal, investment, and accounting advisors before engaging in any transaction. Any third-party information contained herein is from sources believed to be reliable, but which we have not independently verified.